SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

Date of Report (date of earliest event reported): March 23, 2009

SCHLUMBERGER N.V. (SCHLUMBERGER LIMITED)

(Exact name of registrant as specified in its charter)

| Netherlands Antilles | 1-4601 | 52-0684746 | ||

| (State or other jurisdiction of incorporation) |

(Commission File Number) | (IRS Employer Identification No.) |

42, rue Saint-Dominique, Paris, France 75007

5599 San Felipe, 17th Floor, Houston, Texas 77056

Parkstraat 83, The Hague, The Netherlands 2514 JG

(Addresses of principal executive offices and zip or postal codes)

Registrant’s telephone number in the United States, including area code: (713) 513-2000

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| ¨ | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ¨ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ¨ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ¨ | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

| Item 7.01 | Regulation FD Disclosure. |

On March 23, 2009, Andrew Gould, Chairman and Chief Executive Officer of Schlumberger Limited (“Schlumberger”), addressed the oil and gas investment community at the 37th Annual Howard Weil Energy Conference in New Orleans, Louisiana. A copy of the presentation and slides is attached as Exhibit 99.1. Schlumberger has also posted this information on its website at www.slb.com/ir.

The attached presentation contains “forward-looking statements” within the meaning of the federal securities laws, which include any statements that are not historical facts, such as Schlumberger’s forecasts or expectations regarding business outlook; growth for Schlumberger as a whole and for each of Oilfield Services and WesternGeco (and for specified services, products or geographic areas within each segment); oil and natural gas demand and production growth; operating margins; operating and capital expenditures, as well as research & development spending, by Schlumberger and the oil and gas industry; the business strategies of Schlumberger’s customers; Schlumberger’s stock repurchase program; future results of operations and other factors detailed in Schlumberger’s most recent Form 10-K, Form 10-Q and other filings with the SEC. These statements are subject to risks and uncertainties, including, but not limited to, the current global economic downturn; reduction in exploration and production spending by Schlumberger’s customers and reductions in the level of oil and natural gas exploration and development; general economic and business conditions in key regions of the world; operational and project modifications, delays or cancellations; political and economic uncertainty and socio-political unrest; the ability to hire and train new professionals; exploitation of, and changes in, technology; and other risks and uncertainties described elsewhere in the attached presentation, as well as under “Item 1A. Risk Factors” and elsewhere in Schlumberger’s most recent Form 10-K filed with the SEC. If one or more of these risks or uncertainties materialize (or the consequences of such a development changes), or should underlying assumptions prove incorrect, actual outcomes may vary materially from those forecasted or expected. Schlumberger disclaims any intention or obligation to update publicly or revise such statements, whether as a result of new information, future events or otherwise.

| Item 9.01 | Financial Statements and Exhibits. |

(d) Exhibits

The following exhibit is furnished in response to Item 7.01:

| 99.1 | Presentation at 37th Annual Howard Weil Energy Conference |

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| SCHLUMBERGER N.V. | ||

| (SCHLUMBERGER LIMITED) | ||

| By: | /s/ Howard Guild | |

| Howard Guild | ||

| Chief Accounting Officer | ||

Date: March 23, 2009

Exhibit 99.1

3814 words

Ladies and gentlemen good morning—it’s a pleasure to be back in New Orleans and I’d like to thank Paul Pursley and Bill Sanchez for their kind invitation. For the last five years I have stood here and explained that the issue with oil and gas was supply. Luckily, I have never believed in a paradigm shift for commodities so I always made a caveat that the robust demand for oil-field services was subject to there being no major world-wide recession.

Well, now we have that recession, and the game has changed. We are entering a period that will be very different from the last five years when our business was driven by narrow margins of excess supply with resulting effects on oil and natural gas prices. As prices rose so did demand for our services and products—seemingly faster than we could supply—therefore leading to considerable activity growth as well as increases in our prices and costs. As you all know this led to a series of spectacular growth years for Schlumberger.

We should note however, that the increases in oil prices were driven not only by actual demand but also by the perception that demand growth for oil and gas in the non-OECD economies—particularly in China, India, and the Middle East—would continue. We should also note that demand was not limited to oil and gas as all commodities necessary to the rapid industrialization of an economy were subject to similar inflation.

The same picture has not been true for the OECD world where oil consumption has in fact been declining for the last three years. In addition, price has had a direct effect on consumer behavior—particularly for gasoline in the United States—even before the recession.

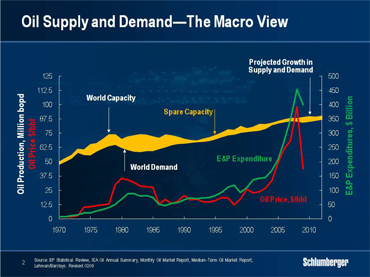

As a result of these factors, the price of West Texas Intermediate which tested $147 in July 2008, ended the year at $45 and has hovered slightly below that level ever since with consequent effect on industry spending plans.

North American natural gas is a different story. The technology and process for the extraction of unconventional gas has evolved so rapidly that the huge increases in rig count seen in 2005 and 2006 have translated in to large production increments. This has now coincided with weaker overall demand and it is going to take time for natural decline to reach a point where any substantial increase in drilling is likely to be needed.

We are now at a stage where the evolution of demand—governed by the level of economic activity—has become the overriding driver of oil and gas price behavior. Over the last few years we have all watched upward and downward revisions of non-OPEC supply. At the present time—and until the world economy stabilizes—we will all be looking for downward demand revisions because these, more than OPEC production cuts, will govern price behavior. Current estimates from the principal forecasting agencies see world demand for oil in 2009 declining by up to 1.4 million barrels a day compared to 2008. However, until GDP estimates stabilize, such figures will be subject to constant revision. For natural gas, the excess of supply over demand will be complicated by the emergence of significant new volumes of LNG at a time when industrial demand everywhere will be at low levels.

Let me be very clear about one thing, this downturn is not about the age of oil being over. On the contrary, oil remains in terms of its energy-to-mass ratio an unrivalled source of energy. Natural gas is not far behind. None of the other sources of energy that the world is working on are anywhere close to oil for its best usage—transportation. Only energy conservation can have a substantial effect on the demand for oil in the medium term, and as long as the population in the non-OECD economies seeks to adopt the lifestyle that the West enjoys, demand for oil is not going to disappear.

So the only question that really needs to be asked is when will demand stop decreasing and stabilize, and when will it start to grow again? When it does, and depending on the length of the current period of reduced investment, we will likely see another period of rapid growth similar to the one that we have just experienced.

Why? Because if you do not explore and invest, production and reserves both shrink. Since I joined the industry, cycles have been growing shorter and shorter. After the 1986 collapse in the oil price for example, and after nine years of heavy investment, the world took nearly twenty years to work off the fifteen million barrels a day of excess production capacity that existed in the mid 1980s. This period would have been shorter but for the exceptional resurgence of production in the former Soviet Union in the early 2000s. Some ten years later, and after the Asian crisis of 1997, oil prices declined to $10 per barrel at the end of 1998 but recovered to $25 at the end the following year. In that cycle activity turned from bust to boom in less than two years.

Such cycles exist also for natural gas where, in North America, surges in drilling and production activity have always been followed by sharp declines as prices fell. The cycle of 2000-2001 was witness to this.

The length of the current downturn depends on the evolution of demand although declines in production and reserves are likely to be felt rapidly. Today’s excess capacity is probably not much more than six million barrels a day, representing less than 7% of the world’s daily consumption—a figure very different from the 25% overhang of the mid 1980s, but very similar to the 6.7% estimated as a worldwide post-peak decline rate by the IEA last year. Obviously, if you do not invest this situation will only get worse.

So what are the likely consequences of this for the industry in both 2009 and beyond?

Well, I will first discuss how the sudden decline in oil and gas prices will affect the spending budgets of our customers that provide us with our revenue. Then I will discuss what this means for Schlumberger.

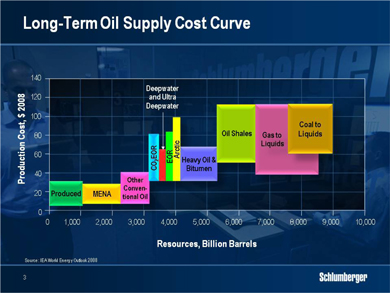

For oil, the cost increases over the last five years—which include increased taxes, commodity inflation and higher service and equipment prices—have meant that only conventional oil and current deepwater projects are profitable at today’s prices. Heavy oil, enhanced oil recovery and ultra-deepwater are not profitable, let alone shale oil or coal to liquids resources. As a result, much of the previously announced Canadian tar sand activity has either been cancelled or delayed, while some National Oil Companies have slowed the development of new heavy oil production.

The price decline has also affected exploration activity, as this can be deferred. This is an important point for Schlumberger to which I will return later.

There is also one other factor accelerating the activity decline and that is the absence of credit. This is particularly the case in the United States and Russia where for different reasons financing has become less available.

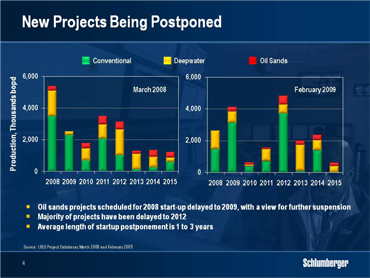

It is becoming increasingly clear, that project cancellations coupled with reduced investment in mitigating decline will rapidly affect supply. Estimates already show an average delay in new project startups from one to three years reducing short-term production capacity by anywhere up to two million barrels per day. This is important in several non–OPEC countries, and in particular Russia, where this will cause the decline rate to accelerate. Certain OPEC countries will also suffer from lower spending levels.

For all of these reasons, the longer the period of lower spending, the more dramatic the fall off in production capacity will be, and the steeper the recovery in oil prices, once demand recovers.

For natural gas, recovery depends on somewhat different factors. These include the large volumes of LNG expected to come to market over the next two years, the improvement in gas transportation infrastructure, and the ability of North America to continue to unlock its unconventional gas resources. Indeed, in North America reduced levels of drilling will be probably be sufficient to sustain unconventional gas production in the short term, but for the service industry, service intensity will grow with more complex wells requiring much higher technology content.

Our industry works in cycles—all of which are all ultimately driven by demand. Periods of intense economic growth or economic stagnation lead to periods of boom and bust in our customers’ investment cycles and we, as suppliers, feel the full effects of such changes in direction. The trick to managing our business is not to think that the state of the cycle either up or down has become permanent. Of course, we all prefer the up cycles but we have learned over time how to profit from the down cycles as well.

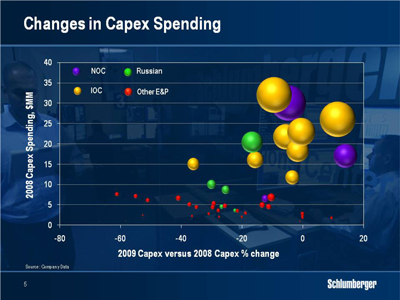

The changes that I have just described do not apply universally across the customer portfolio. While not every company has announced their intentions, the international oil companies are generally not making substantial cuts although they will seek lower service pricing to try to bring project economics in line with lower commodity pricing. The budgets of the national oil companies are mixed, but several—particularly the Chinese—have announced continued high levels of investment. The rest have all announced cuts of varying size but it is particularly noticeable that the largest reductions tend to be in Canadian heavy oil or in Russia—two areas that I mentioned earlier. This chart of course will evolve as the year progresses as a function of oil and gas prices.

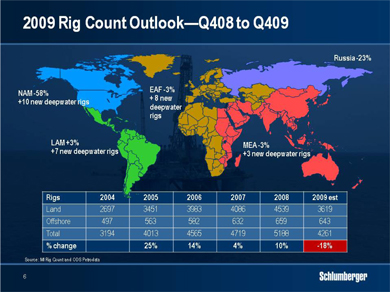

Translating capex reductions into rig count leads to this estimate of rig count from the fourth quarter of 2008 to the fourth quarter of 2009. This will still be subject to huge fluctuations in oil and gas prices over the remainder of the year but certain trends are apparent. Offshore, activity will only decline marginally as new deepwater rigs come on contract although some jack-ups and shallow-water semi-submersibles will be stacked. On land, the largest declines will be in North America and Russia while Latin America will show a marginal increase and Europe, Africa and Middle East will remain stable or decline only slightly.

I would caution you that this picture can change considerably over the rest of the year.

One final element of today’s scenario is the short-term effect of activity declines on pricing. Our customers have all seen huge inflationary price increases over the past five years. This has resulted from general commodity inflation, shortages resulting from pent-up demand, and project inefficiencies due particularly to lack of skilled personnel. Our customers are now determined to remove some of that inflation from their service providers to bring project economics more in line and are requesting re-negotiation of existing contracts and trying to trade volume or extended duration against price. The threat is that prices will be even lower in a new tender. Similarly, we are equally trying hard to reverse some of the cost increases we have incurred from our suppliers over the same period. The whole process of cost and price re-adjustment will take from twelve to eighteen months and will depend on how activity levels evolve.

So now I’m going to discuss for what these vastly changed circumstances mean for Schlumberger. I will start with the three most adversely affected elements of our business.

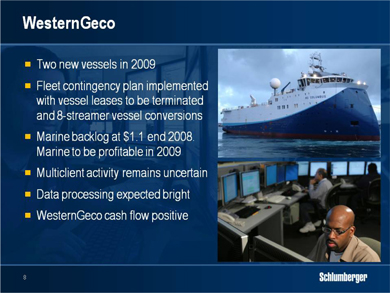

First, our seismic company WesternGeco will be heavily affected by the reduced exploration spend. When we bought Eastern Echo, we made a contingency plan to cover reduced activity and we are now implementing this plan. We have just taken delivery of the first Eastern Echo vessel—the WesternGeco Columbus—and we will launch a second later this year. We will now be able to terminate the leases on most of our source vessels during the year and convert some of our older 8-streamer boats to source vessels. As a result, by the end of 2009, nearly all of our fleet will be fully owned yet we will retain the capability to react to increasing activity quickly and cost-effectively.

We began the year with a strong Marine backlog of just under $1.1 billion—part of the total $1.8 billion backlog reported. Customer enquiries have since declined but so has the number of new seismic vessels that will actually be completed. We therefore expect Marine to remain profitable in 2009.

The big uncertainty will be the level of multi-client activity, particularly in the Gulf of Mexico. We will continue to insist on significant pre-funding for new surveys but we will also remain cautious in our outlook on customer spend. The one bright spot is in data processing where Reverse Time Migration algorithms and Full Wave Form inversion technology are creating new markets.

Overall, WesternGeco operating cash-flow will remain positive in 2009 but it will nevertheless be a tough year for results.

In Russia, activity declines will be amplified by the devaluation of the Russian rouble against the US dollar. We expect IOC activity to remain strong while activity in Western Siberia will be weak in the first half before recovering somewhat towards the end of the year. Land activity decline in Russia will be second only to the US, but falling production and slowing new development will make this a prime market again once oil prices recover and credit markets ease. We will profit from this period to further integrate the companies we acquired during the last upturn and to considerably reduce our cost base.

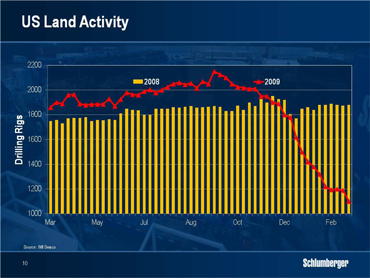

In US Land we do not expect a substantial recovery in the second half year as natural gas demand will likely require only low levels of drilling through the end of the year. Service intensity associated with complex well geometries and multi-stage fracturing and completion operations will increase and support activity although pricing will remain extremely competitive. While the big question remains as to how soon the reduced rig count will lead to production decline, we do not expect any significant change before 2010.

Now that I have dealt with the three most difficult parts of our portfolio I need to point out the positives. We are encouraged to see deep-water activity largely unchanged, in spite of expected changes in our customers’ exploration spending. As this affects service intensity, I would point out although some of these rigs may now move to delineation or early development work, the services that are required still demand a high proportion of the measurement-based technologies in which Schlumberger excels. In other areas, positives include robust natural gas activity in the Middle East, and strong activity in Latin America and parts of the Far East.

Let me turn to the management of the company in the downturn.

The short-term actions fall into three categories. The first is good housekeeping, which implies adjustment of our costs to lower levels of activity and pricing. We have already announced a headcount reduction of 5%, which we will have largely completed by the end of the first quarter, and a further reduction of a similar amount is likely over the coming months. We have removed some of the variable compensation mechanisms introduced to retain employees in the rapid growth phase, and we have cut a lot of staff functions and reduced or cancelled many non-essential projects. We have also removed some levels of management and we are reemphasizing control over much discretionary cost.

Secondly, capital expenditure. The majority of our capex is focused on new equipment for field deployment. Some of this is replacement equipment; some is in support of new products and services. A down cycle provides the opportunity to consolidate and prepare for the next period of growth and we can afford to be economical because we are not introducing a large amount of equipment in response to growth. We currently estimate that our capital expenditure for 2009—including multi-client surveys capitalized—will approximate $2.9 billion.

Thirdly, the supply chain organization has had to become very savvy, very quickly. We use a lot of complex parts and sub-assemblies in our equipment that must be sourced, qualified, manufactured, and deployed. Sub-contractors are important, and it’s essential that we help them manage the downturn almost as much as we help ourselves. At the same time we have the same issue as our customers in driving out some of the accumulated inflation in our supply chain. This takes time and realistically it will be a year before the effects work their way through the system.

At the same time there are certain investments that need to be protected to ensure the company maintains its capacity to respond when activity turns around. The first of these is people. In the last five years we have recruited 11,613 engineers in 140 countries from 200 different universities. We have also recruited 8,574 specialists who perform many of the complex well site tasks such as stimulation, well testing and completions. In the same period, we have invested in two new state-of-the-art training centers with capital cost in excess of $200 million and have conducted more than 1.3 million training days.

The cuts that we have announced therefore come after a period of tremendous growth and are relatively easy to make. We will still continue some recruiting—we have all learnt the lesson of the 1980s when the lack of attention paid to hiring new talent left us with a missing generation of managers and experienced professionals, not to mention an exceedingly poor reputation on campus.

We also know that retiring baby-boomers still have to depart in large numbers. Managing their retirement, while not cutting too deeply into recent recruits, will be essential to having a qualified workforce when activity returns. If the investment in recruiting and training has been substantial since 2004, then the investment in competency development must be just as substantial right now.

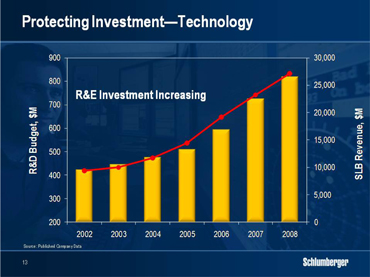

The second investment that Schlumberger has always protected in downturns is that in research and engineering. Today’s investment provides the fuel for the technology of tomorrow. The age of easy oil is gone and careful management of research and engineering investment is essential. We have traditionally not cut such investment during downturns and we will not do so this time. This has always allowed us to emerge from each downturn with a refreshed and stronger portfolio of products and services.

There are also other strategies to ensure that the company comes out of the downturn changed and more competitive. Our customers are executing more difficult and much larger projects in more remote locations. This implies huge advances in technology to be able to recover hydrocarbons cost effectively. It also implies that the value of reliability in operations to our customers has increased dramatically. In the future service quality will be a major differentiator. The savings in time and cost for both our customers and ourselves are potentially enormous.

We therefore launched at the end of 2007 a program called “Excellence in Execution” with a goal to deliver flawless execution to our customers. There are two parts in achieving this objective.

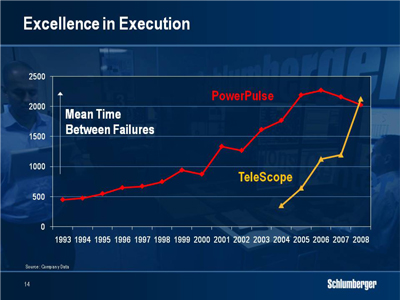

First, it requires a step change in the reliability of our products and services. For this, we have created an Engineering, Manufacturing, and Sustaining organization to establish systems, processes, and standards across all of our product development and manufacturing centers worldwide. This will enable us to design for reliability as well as for manufacturability and maintenance, while manufacturing for zero defects. This is obviously a long-term effort with the potential for enormous results. As an example, take a look at two successive generations of while-drilling telemetry. The first of these, PowerPulse, was introduced in 1993 and until recently formed the main part of our service fleet. Look at how long it took to realize the reliability potential—measured in average hours between failures. Its successor, TeleScope, initially suffered the same low reliability level but a new approach boosted its performance to that of its predecessor much more rapidly. From 2009 on, we expect future technology generations to begin where previous generations left off, not by returning to an initial lower level.

The second part of Excellence in Execution is to make a step change in our service delivery performance. For this, we have introduced a separate quality organization. We want to evolve our strong ‘can-do’ culture to a ‘we can do it right the first time every time” approach. This implies the upgrading of our systems and procedures, as well as a major overhaul of our maintenance facilities, procedures and training.

Excellence in Execution is a multi-year initiative that will not be abandoned for short-term cost considerations.

Finally, I’d like to turn to the balance sheet. At the end of 2008 we had net debt of $1.13 billion and available committed unused bank facilities of $1.8 billion. Cash flow generation will be strong in 2009. We have made several acquisitions over the last five years although generally we slowed the rate at which we acquired companies as valuations rose. Such valuations are now falling more into line and we can be more opportunistic than we have been.

In conclusion, we are in a period where the dynamic of our industry has switched from that of supply to demand. However, as I pointed out, oil supply is particularly vulnerable to reduced investment and as soon as demand stabilizes or starts to grow again there will be new tension on the supply side. The longer the downturn lasts the more acute that tension will be. Of course, judging the moment demand will turn is still almost impossible and your estimate is as good as anything I might say as it depends on the general economy. This is equally true of gas with the probability that the rapid increases in supply mean that the down cycle will last longer than for oil.

In these circumstances our management will be concentrating on short-term actions to ensure we minimize the effect of the down cycle on our overall profitability while continuing the programs in people, technology and process that we know will benefit us in the long term. We have always been prudent in our cash management and we will continue to be so. We have suspended our stock repurchase program but have maintained our dividend. We will actively seek acquisitions at attractive valuations and I remain convinced that we will emerge from this downturn, as we have emerged from previous downturns, a stronger and better company.

Ladies and gentlemen, thank you for your attention.